in Focus

What We Must Monitor

In An Era of Unprecedented Uncertainty

The global economy is entering a level of uncertainty that exceeds both the 2008 global financial crisis and the COVID-19 pandemic. In addition to trade risks triggered by the aggressive tariff policies of the second Trump administration, the recent outbreak of war between the United States and Iran is effectively resetting the trajectory of the global economy. In Korea, the combined impact of higher oil prices, a stronger US dollar and inflationary pressures is expected to intensify, as the country is highly dependent on energy imports. Against this backdrop, this article examines the key economic trends and indicators that must be closely monitored to navigate the current environment.

By Joon-young Hur, Professor of Economics, Sogang University

That we are living in an “era of uncertainty” may always be an apt description. In the aftermath of the 2008–2009 global financial crisis, uncertainty stemmed from the shock of the crisis itself, while in the wake of the COVID-19 pandemic in 2020, it reflected the unprecedented disruption caused by a global health emergency.

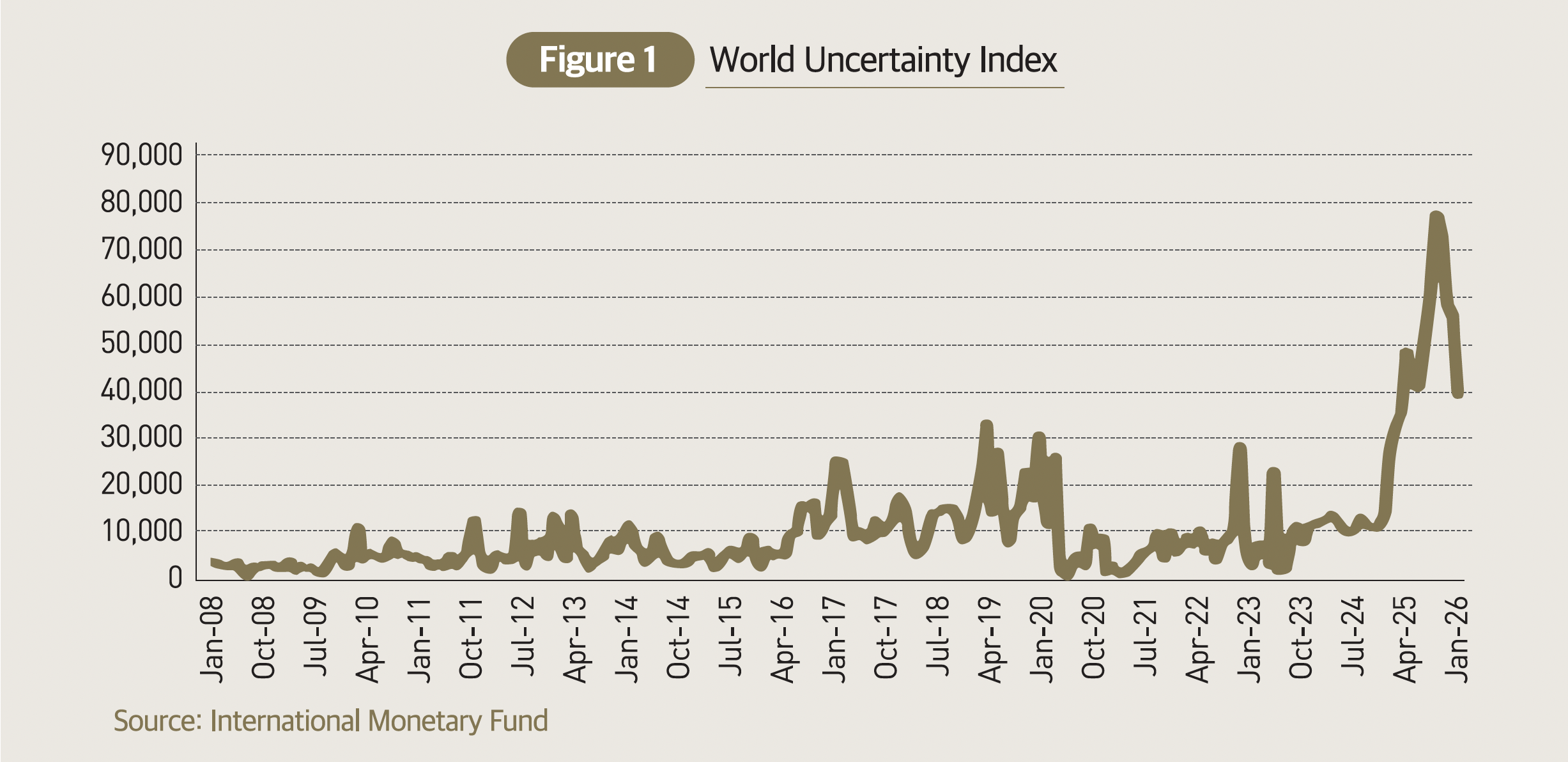

How, then, does the level of uncertainty we face in 2026 compare with previous periods, and what are its sources? To address this question, the World Uncertainty Index compiled by the International Monetary Fund from 2008 onward is shown in [Figure 1]. The index rose sharply after 2025 and, although it has declined from its peak in April 2025, the index remains significantly higher than levels observed following the global financial crisis or the pandemic.

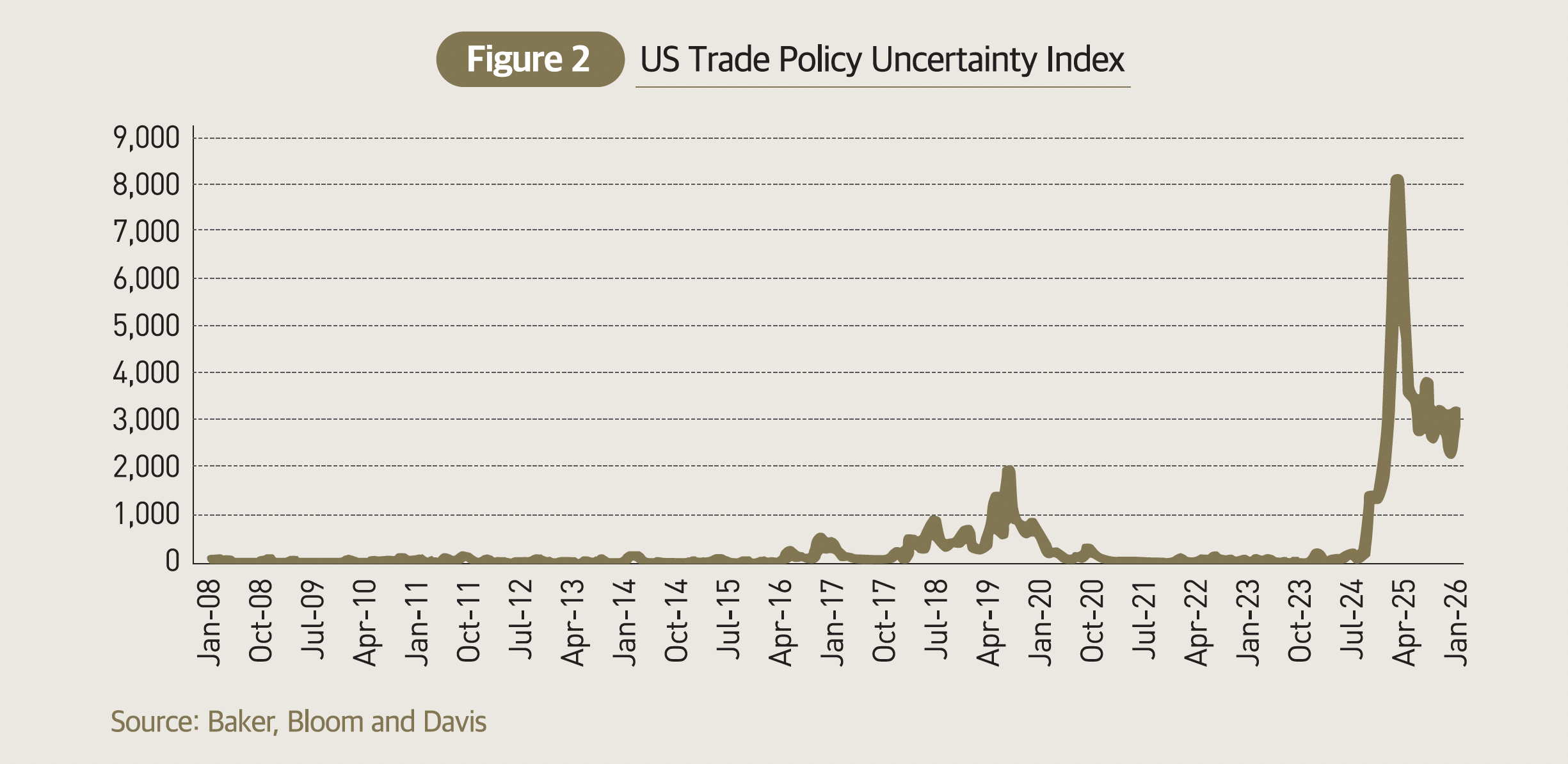

[Figure 2] provides further insight into the sources of this uncertainty. The US Trade Policy Uncertainty Index, developed by renowned economists Baker, Bloom and Davis, increased sharply from just before the inauguration of the second Trump administration in January 2025 and reached its peak in April 2025, when reciprocal tariffs were announced on a global scale. The index began to decline as countries subsequently engaged in renegotiations with the United States to reduce these tariff rates. The recent trajectory of US trade policy uncertainty closely mirrors the movement of the World Uncertainty Index shown in [Figure 1].

In effect, the current elevated level of global uncertainty can be attributed in large part to the trade policies of the second Trump administration. This has been compounded by the US Supreme Court ruling in early 2026 that tariffs imposed under the International Emergency Economic Powers Act (IEEPA), including reciprocal tariffs and fentanyl-related tariffs, exceeded presidential authority, which added a new layer of uncertainty. Nevertheless, the administration’s commitment to maintaining tariff measures appears firm. In the near term, a global tariff of 10–15% on imports under Section 122 of the Trade Act is likely to be imposed as a substitute for reciprocal tariffs. Before the expiration of this provision within 150 days, there may be investigations into unfair trade practices by partner countries to introduce additional tariffs under Section 301 of the Trade Act or Section 232 of the Trade Expansion Act. As uncertainty over the scope and structure of these measures increases, the US Trade Policy Uncertainty Index rose from around 2,250 in January 2026 to nearly 3,150 in February.

Alongside trade policy uncertainty, the outbreak of war between the United States and Iran in early March 2026 has further deepened global uncertainty. Reportedly, the strategic outline of the conflict from the US and Israel's point of view involved three phases: first, the removing Iran’s core leadership; second, large-scale airstrikes aimed at neutralizing ballistic missiles, drones and air defense systems; and third, the removal of regime-supporting forces, including the Revolutionary Guard, with the objective of establishing a new government. One week into the conflict, operations appear to be in the second phase, and the duration and intensity of the war will likely depend on whether or not the third phase is entered, as well as whether ground operations will be initiated. Financial markets are increasingly reflecting the possibility of a prolonged conflict. International oil prices, in Brent crude terms, rose from the low USD 70s range per barrel prior to the outbreak of hostilities to above USD 90 within a week. While the three major US stock indices declined, the demand for safe-haven assets increased, which drove up US dollar and gold prices. The economy detests uncertainty and as uncertainty rises, firms tend to scale back capital investment and households reduce consumption. Financial market volatility increases, particularly in equity markets, and exchange rates become unstable. These factors are expected to exert downward pressure on both the global economy and the Korean economy, but the magnitude of their impact will depend on the direction of US trade policy and the evolution of the US–Iran conflict. Thus it is difficult to make definitive projections at this stage.

Nonetheless, the most appropriate approach to assessing future prospects for the global and Korean economies is to return to baseline forecasts established prior to these developments and adjust them to reflect recent changes.

At the beginning of this year, global economic projections for 2026 presented by international organizations such as the IMF and the OECD can be summarized as follows. Global growth was expected to remain in the low-3% range, broadly in line with the pre-pandemic 10-year average of 3.1%, despite US trade policy developments. Among advanced economies, the US was projected to maintain relatively strong growth, while Europe was seen as gradually recovering from a period of weakness, and China’s growth was expected to moderate amid continued challenges in the real estate sector. In terms of US trade policy, it was anticipated that the Trump administration, facing midterm elections in November, would refrain from implementing aggressive tariff measures that could place additional pressure on the domestic economy, particularly through inflation. These projections, however, did not incorporate the possibility of a US–Iran conflict.

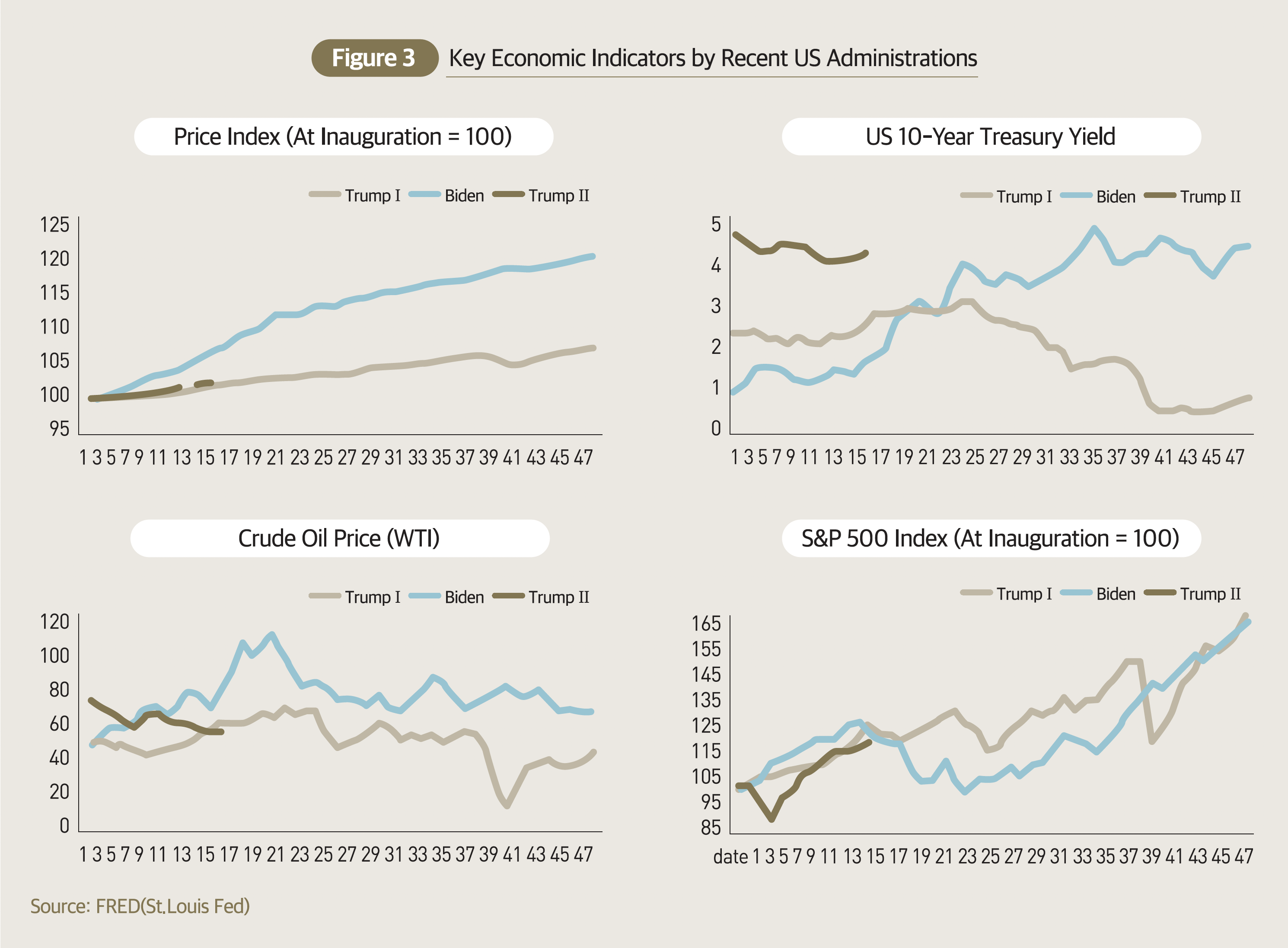

Turning first to the factors behind rising uncertainty in US trade policy, the economic backdrop to the second Trump administration can be characterized by a “low-inflation, low-interest-rate, low-oil-price” environment. As shown in [Figure 3], inflation during the first Trump administration remained lower than during the Biden administration, with cumulative increases of 7.6% and 20.9%, respectively, while market interest rates also stayed relatively low after the initial phase of the term. Oil prices likewise remained lower throughout the Trump administration than under the Biden administration. Given that elevated inflation became a central domestic issue during the Biden years, the current administration is likely to face constraints in pursuing tariff policies that could further stimulate inflation ahead of the midterm elections. In this context, the near-term likelihood of aggressive tariff measures being implemented, following the US Supreme Court ruling that the tariffs imposed under the IEEPA exceeded presidential authority, appears limited.

A more pressing concern is the potential for a prolonged conflict between the United States and Iran. Rising oil prices driven by geopolitical risks in the Middle East would run counter to the economic policy outlook of the Trump administration. According to the IMF, a 10% increase in oil prices would reduce global economic growth by approximately 0.15% and raise inflation by about 0.4% in the following year. This dynamic would also weigh on the US economy. Bloomberg has recently projected that under a worst-case scenario in which the conflict becomes prolonged, oil prices could reach USD 108 per barrel by year-end, while US inflation could rise to 3%.

Recent declines in presidential approval ratings and a loss in a Senate election in Texas suggest that the midterm elections are emerging as a key political constraint for President Trump. A plausible risk scenario could emerge if the Trump administration were to prioritize short-term political considerations less and instead allow the conflict to persist. In such a case, the economic outlook would deteriorate significantly. Prolonged conflict would drive further increases in oil prices and intensify inflationary pressures in the US, reducing the likelihood of interest rate cuts by the Federal Reserve and weakening market expectations for monetary easing. This would place additional strain on AI-related investment, tighten financial conditions and potentially trigger corrections in US equity markets. Ultimately, even the US economy, which was among a handful of advanced economies expected to maintain relatively strong growth, would face increasing downward pressure.

The key issue for Korea is the extent of the burden the economy would bear if such a scenario materializes. According to the Hyundai Research Institute, Korea recorded the highest oil consumption per USD 10,000 of GDP among OECD member countries, at 5.63 barrels, as of 2024. With annual energy import costs exceeding USD 100 billion, rising oil prices would increase inflationary pressure, weaken the current account balance and ultimately weigh on economic growth. In addition to the direct impact of higher oil prices, a stronger US dollar driven by heightened global demand for safe-haven assets would represent another adverse factor for the Korean economy.

Even in a period of heightened uncertainty, economic activity must continue. As discussed, the most significant near-term source of uncertainty is geopolitical risk in the Middle East, underscoring the importance of continuous monitoring. In practice, this may require closely tracking daily movements in US equity markets, developments in oil prices and fluctuations in the US dollar index and the KRW–USD exchange rate.