in Focus

Survey on the Current Status and Outlook of Competitiveness

Among Korea, the United States, Japan, and China

Across All Industries by 2030

Chinese companies competing with Korea’s major export industries are no longer merely playing catch-up, but are entering a phase of overtaking Korean firms. According to the Survey on the Current Status and Outlook of Competitiveness Among Korea, the United States, Japan, and China,1 conducted by FKI, many leading firms believe that Korea trails China in a significant number of industries. Looking ahead to 2030, respondents expect China to hold a competitive advantage across all ten of Korea’s key export industries. At a time when global competition is increasingly defined by U.S.-China dominance and rivalry, there is an urgent need for a strategic response from Korea.

Compiled by Na-yeon Kim

Photo Credit FKI

- 1.The survey was conducted among Korea’s top 1,000 companies by sales operating in ten major export industries. A total of 200 companies responded. The industries include semiconductors, displays, electrical and electronic equipment, automobiles and auto parts, general machinery, shipbuilding, secondary batteries, steel, petrochemicals and petroleum products, and biohealth.

Sustained U.S. and China Advantage Over Korea

Corporate perceptions of national competitiveness clearly reveal Korea’s sandwiched position between the United States and China. Setting Korea's competitive level as a baseline of 100 for 2025, respondents rated the United States at 107.2, China at 102.2, and Japan at 93.5. Looking five years ahead, the projected figures rise to 112.9 for the United States and 112.3 for China, while Japan edges up only to 95.0. These results indicate that:

- Korean firms already perceive themselves as operating at a lower level of competitiveness than both U.S. and Chinese companies.

- The gap with the United States and China is expected to widen further, while Korea’s competitive edge over Japan is projected to narrow.

China’s trajectory is particularly notable. By 2030, China is expected to reach a level of competitiveness virtually on par with the United States. Korean companies increasingly view China not only as their most immediate competitor, but also as a country poised to compete directly with the United States for global leadership.

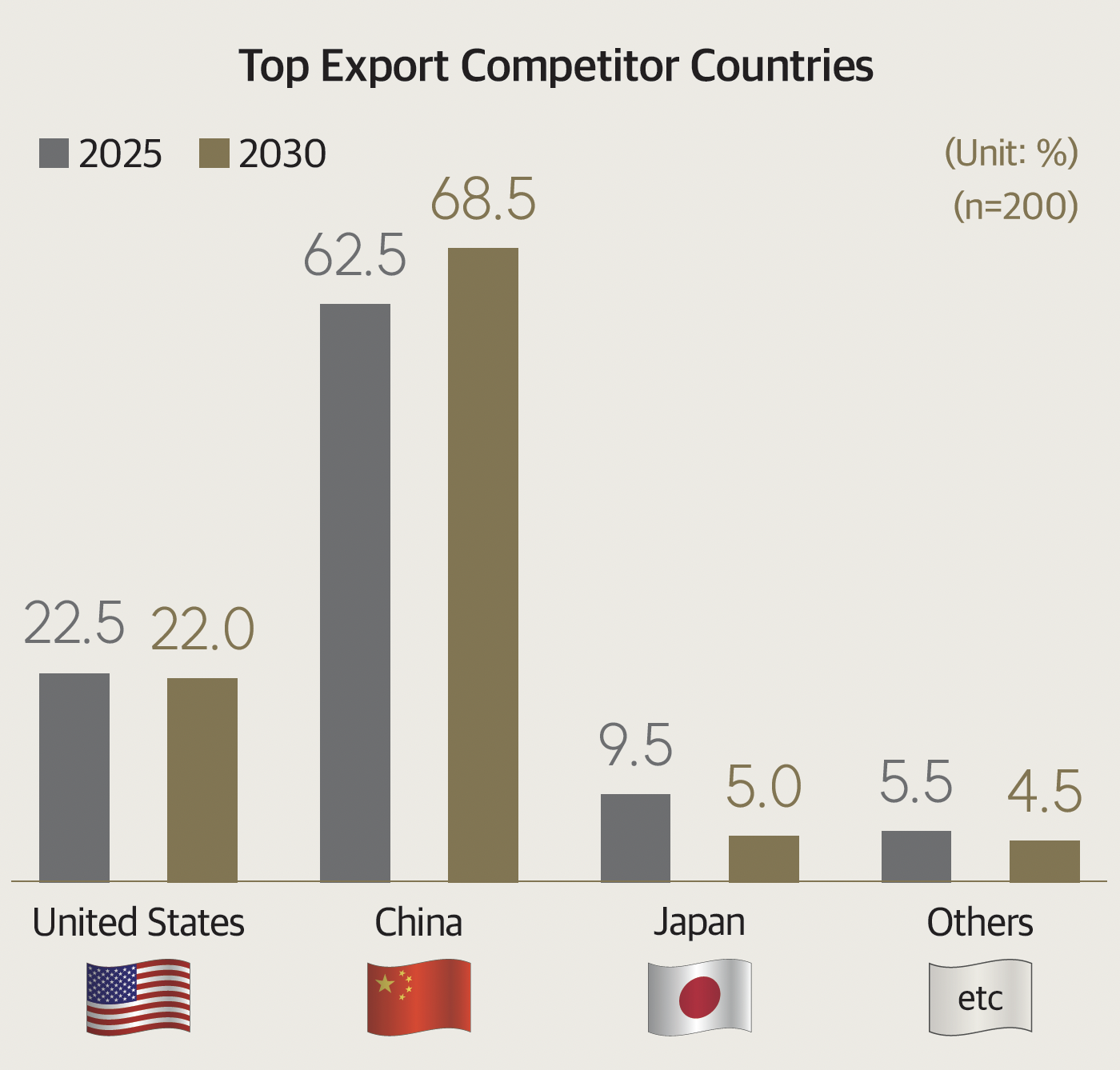

Intensifying Export Competition with China

According to the survey, 62.5% of Korean companies identified China as their largest export competitor in 2025. This share is expected to rise to 68.5% by 2030, pointing to intensifying competition.

By contrast, the share of respondents citing the United States as their main competitor remains largely flat at 22.5% in 2025 and 22.0% in 2030, while Japan declines from 9.5% to 5.0%. These trends suggest that:

- Export competition is becoming increasingly concentrated around a Korea-China dynamic.

- Korean firms already perceive China as the most realistic and threatening competitor in the field, and expect the competitive burden to grow even heavier in the years ahead.

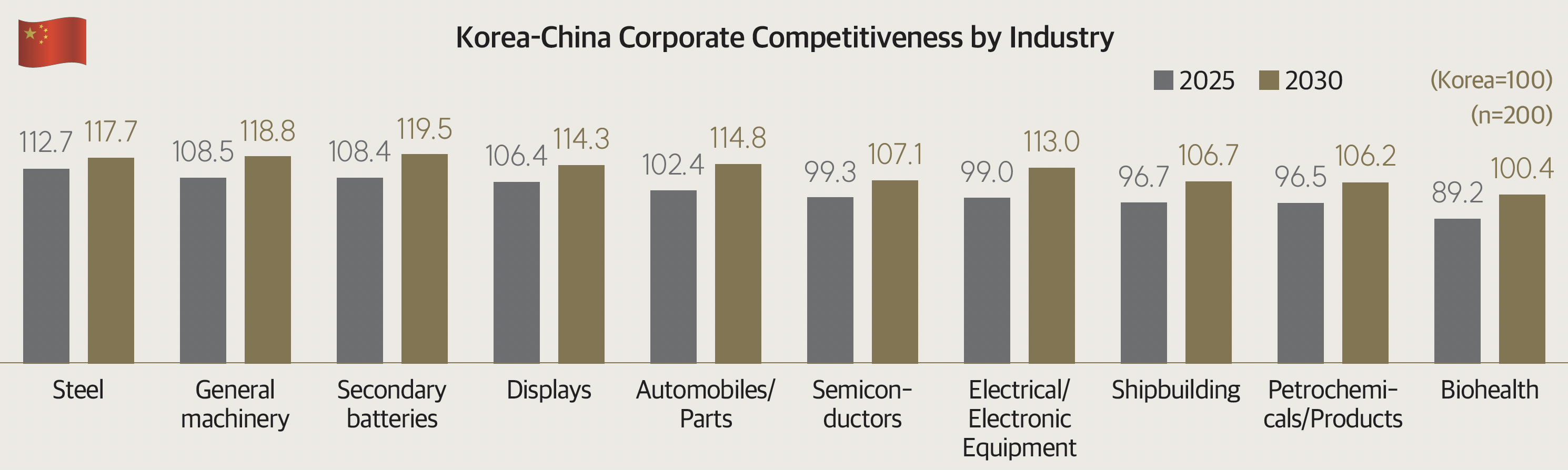

Semiconductors and Electronics Perceived to be at Risk

An industry-by-industry outlook reveals a more pronounced structural challenge. As of 2025, China already outperforms Korea in five of the ten key export industries, including steel (112.7), general machinery (108.5), secondary batteries (108.4), displays (106.4), and auto parts (102.4). Korea currently maintains an edge in five sectors, including semiconductors (99.3) and electrical and electronic equipment (99.0). The outlook for 2030, however, is markedly different. Survey respondents expect that:

- China will surpass Korea in competitiveness across all ten major export industries by 2030.

- Even high-technology and high-value-added sectors such as semiconductors and electrical and electronic equipment, long regarded as the final strongholds of Korean manufacturing, could be overtaken.

These expectations reflect a reality in which China is expanding its sphere of industrial competitiveness and is encroaching on areas where Korea maintains a comparative advantage.

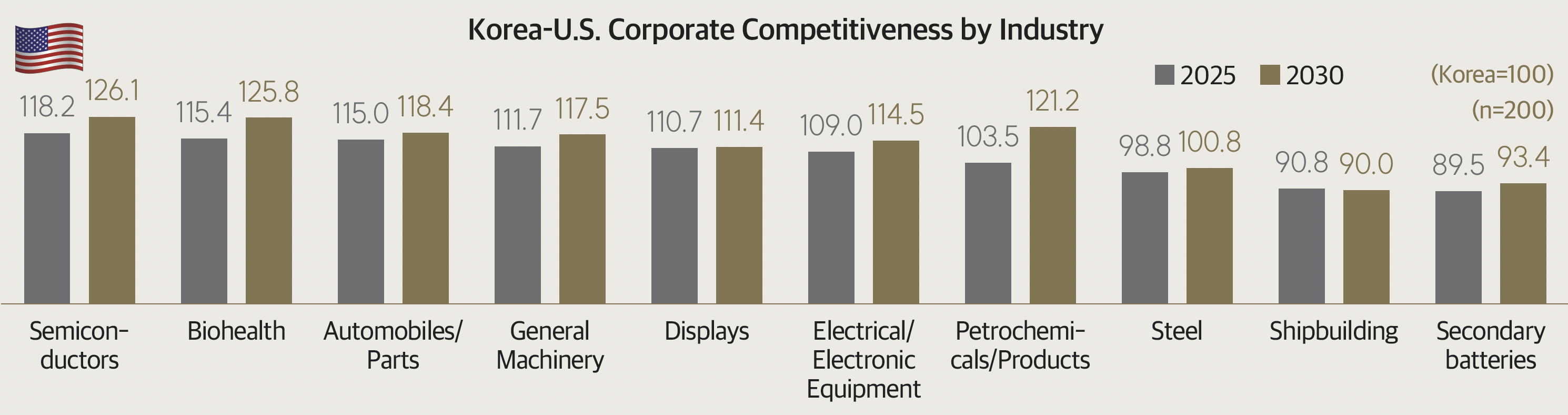

Korea’s Leading Industries Narrow from Three to Two

As of 2025, Korea holds a competitive advantage over the U.S. in three industries: steel, shipbuilding, and secondary batteries. In contrast, the United States holds a clear advantage in seven industries including semiconductors (118.2) and biohealth (115.4). The outlook for 2030 suggests that this gap will widen further.

- Steel is expected to fall behind the United States, leaving only shipbuilding (90.0) and secondary batteries (93.4) as the only two industries where Korea retains a relative advantage.

- There is growing concern that gaps will continue to expand under a competition that is based on brand strength and technological leadership.

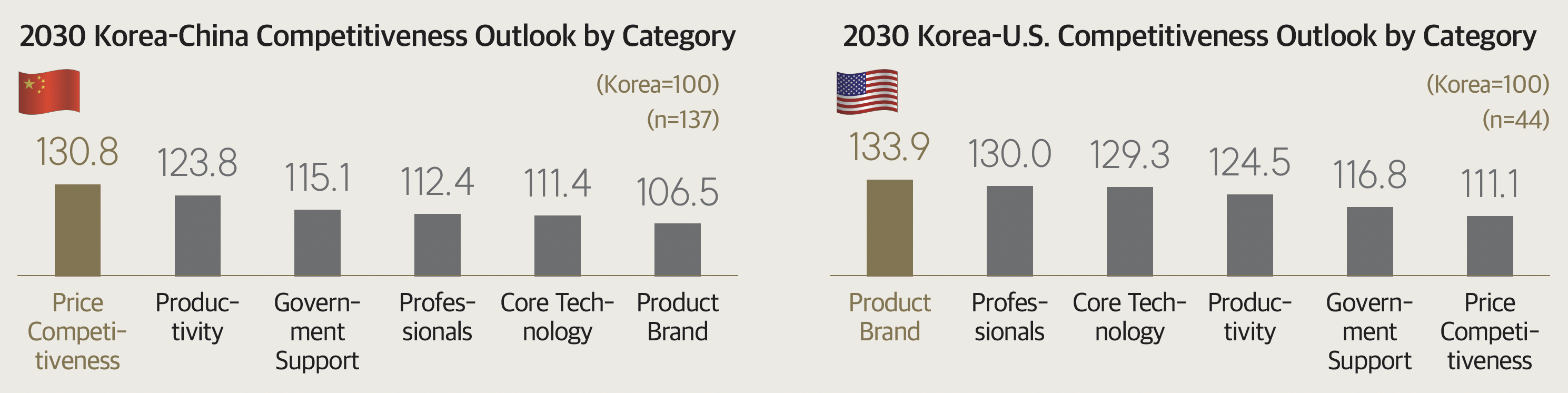

China Expands Its Lead, the United States Maintains Structural Dominance

A comparison of competitiveness by category shows that China already outperforms Korea in areas such as price competitiveness (130.7→130.8) and productivity (120.8→123.8).

- At present, Korea holds a comparative advantage over China in product branding only, among a total of six categories. Five years from now this advantage too is expected to fade.

- These results indicate that China is no longer merely a low-cost production base, but has evolved into a comprehensive competitor with strengths in production efficiency, policy support, and industrial ecosystems.

Companies that identified the United States as their primary competitor responded that the U.S. advantage will strengthen further in product branding (132.0→133.9), professional talent (126.2→130.0), and core technologies (124.0→129.3).

This suggests that Korean firms increasingly view gaps with the United States in branding, R&D capability, and global talent acquisition as structural challenges. Rather than short-term fixes, companies are seeking long-term strategies centered on technology investment, talent development, and brand building.

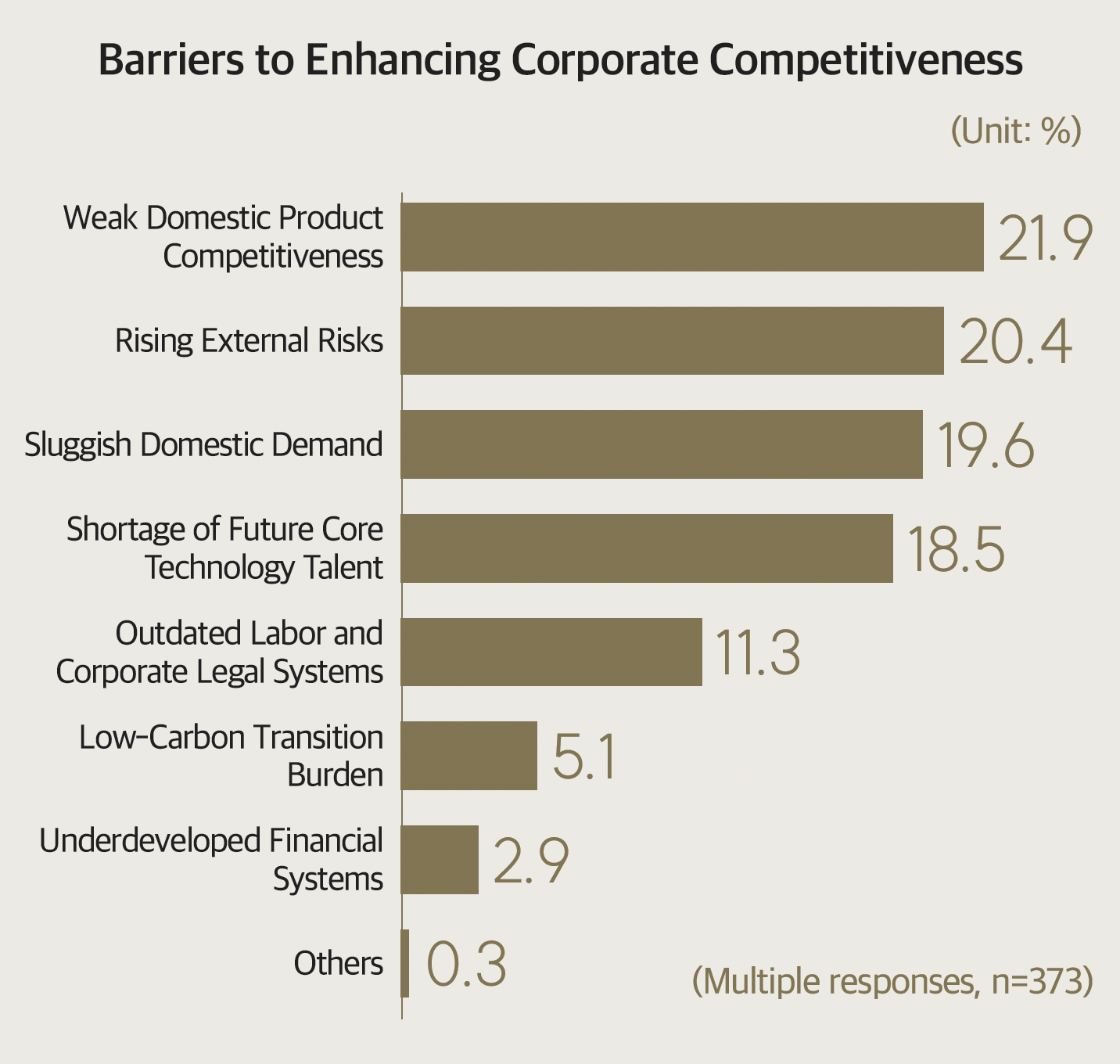

Weakening Product Competitiveness and External Risks are the Greatest Burdens

What do companies see as the greatest constraints on competitiveness at the operational level? Respondents identified weakening domestic product competitiveness (21.9%) as the most significant constraint, followed by rising external risks such as protectionism (20.4%), sluggish domestic demand due to population decline (19.6%), shortages of talent in future core technologies such as AI (18.5%), and outdated labor markets and corporate legal frameworks compared with competitor countries (11.3%).

- In other words, external competitive pressures from China and the United States, and

- Domestic structural issues including low growth, demographic decline, and regulatory constraints are simultaneously weighing on corporate competitiveness.

In particular, while declining product competitiveness and talent shortages are challenges firms must address themselves, institutional factors such as regulation, labor markets, and taxation are difficult to improve without government action. This underscores the need for coordinated public-private strategies.

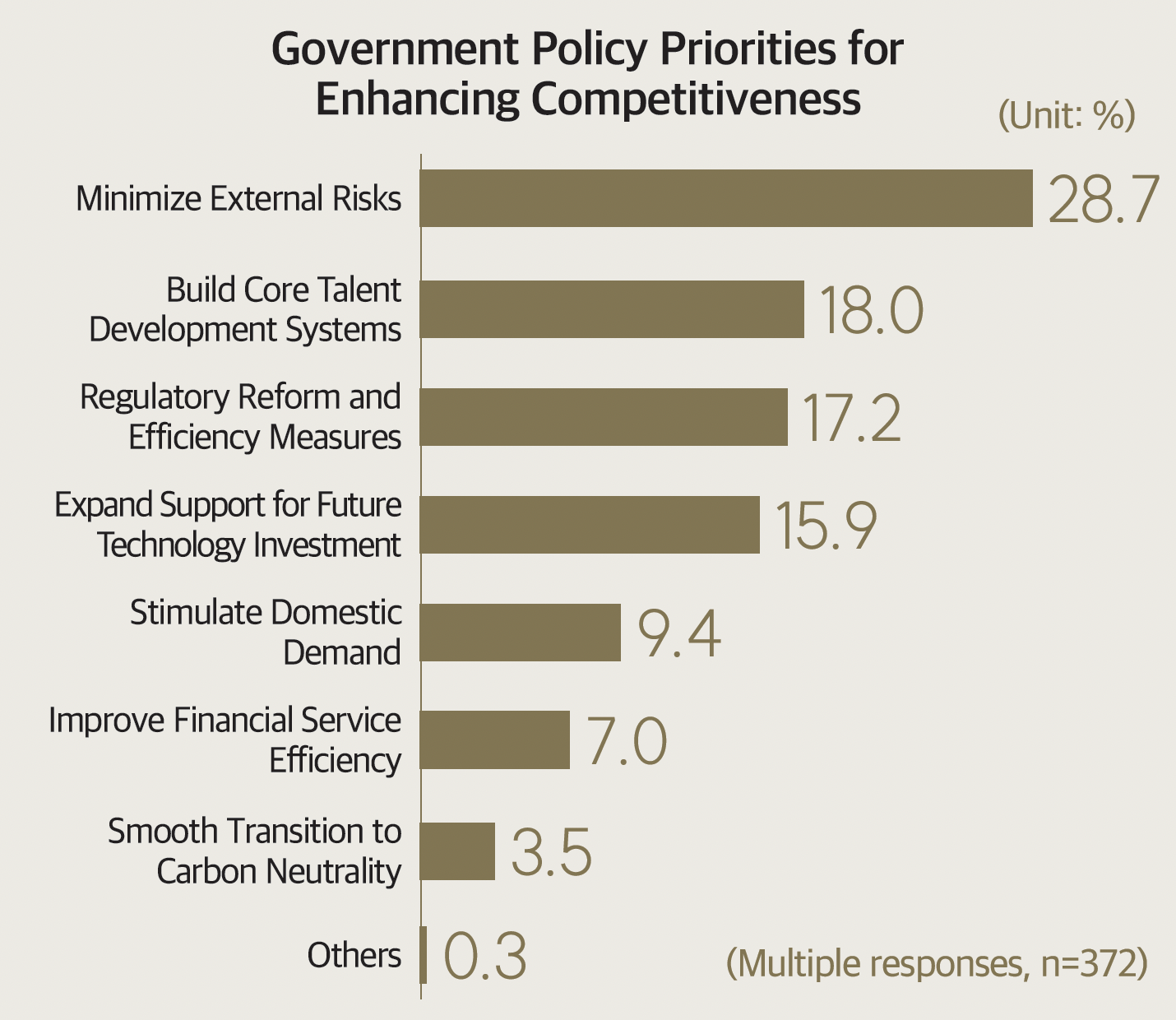

A Robust Policy Foundation Is Essential

Companies preferred government action are relatively straightforward. Priority policies to boost competitiveness include: minimize external risks (28.7%), build systems for developing core talent (18.0%), improve economic efficiency through reasonable taxation, regulatory reform, and labor market flexibility (17.2%), and expand support for future technology investment (15.9%).

Amid an increasingly uncertain global economic environment, companies are calling for:

- A safety net to withstand external shocks, and talent, technology, and institutional infrastructure capable of supporting long-term growth.

This survey provides a stark snapshot of the competitive environment facing the Korean economy. Competition with China is evolving into a race with gaps being widened over time, while structural gaps with the United States in technology and talent continue to accumulate. Corporate self-help efforts alone are unlikely to be sufficient, and a comprehensive competitiveness strategy is required, linking external risk management, core talent development, regulatory reform, and investment in future technologies.