2026 Economic and Business Environment Outlook

Korea’s Economy in 2026

Finding a New Balance in an Era of Low Growth

In 2026, Korea’s economy moves beyond a low-growth phase, but enters a turning point marked by widening disparities in recovery across industries. The article examines Korea’s pathway for future growth amid coexisting expectations for easing and structural constraints.

By Seung-suk Lee, Senior Research Fellow, Korea Economic Research Institute (KERI)

Korea’s economy in 2026 stands at the midpoint of a transitional phase, where multiple forces collide and are reconfigured simultaneously. After enduring prolonged high interest rates, exchange rate volatility, adjustments in real estate and project finance, and a slowdown in global trade throughout 2025, the economy is gradually emerging from its trough. However, the rebound is not taking the form of a vigorous cyclical upswing seen in past recoveries. Instead, it resembles a phase of “transitional normalization,” in which multiple constraints and new growth drivers operate in parallel.

The global environment also serves as a test of Korea’s economic resilience. The United States is approaching a soft landing, but the expansion of government bond issuance driven by large fiscal deficits is preventing a decline in long-term interest rates. Even with policy rate cuts and the announcement of an end to Quantitative Tightening (QT)1, the shock-absorbing capacity of financial markets has weakened, leaving room for increased volatility. At the same time, strong AI investment momentum and elevated valuations, alongside slowing growth in China and Europe, present both opportunities and challenges for Korea’s economy.

Against this backdrop of intersecting forces, 2026 is expected to be a pivotal year—going beyond short-term recovery to define Korea’s pathway for medium- to long-term growth.

- 1.QT: A tightening policy in which central banks reduce liquidity by shrinking holdings of assets such as government bonds and MBS. It is used as a key monetary tightening tool alongside policy rate hikes.

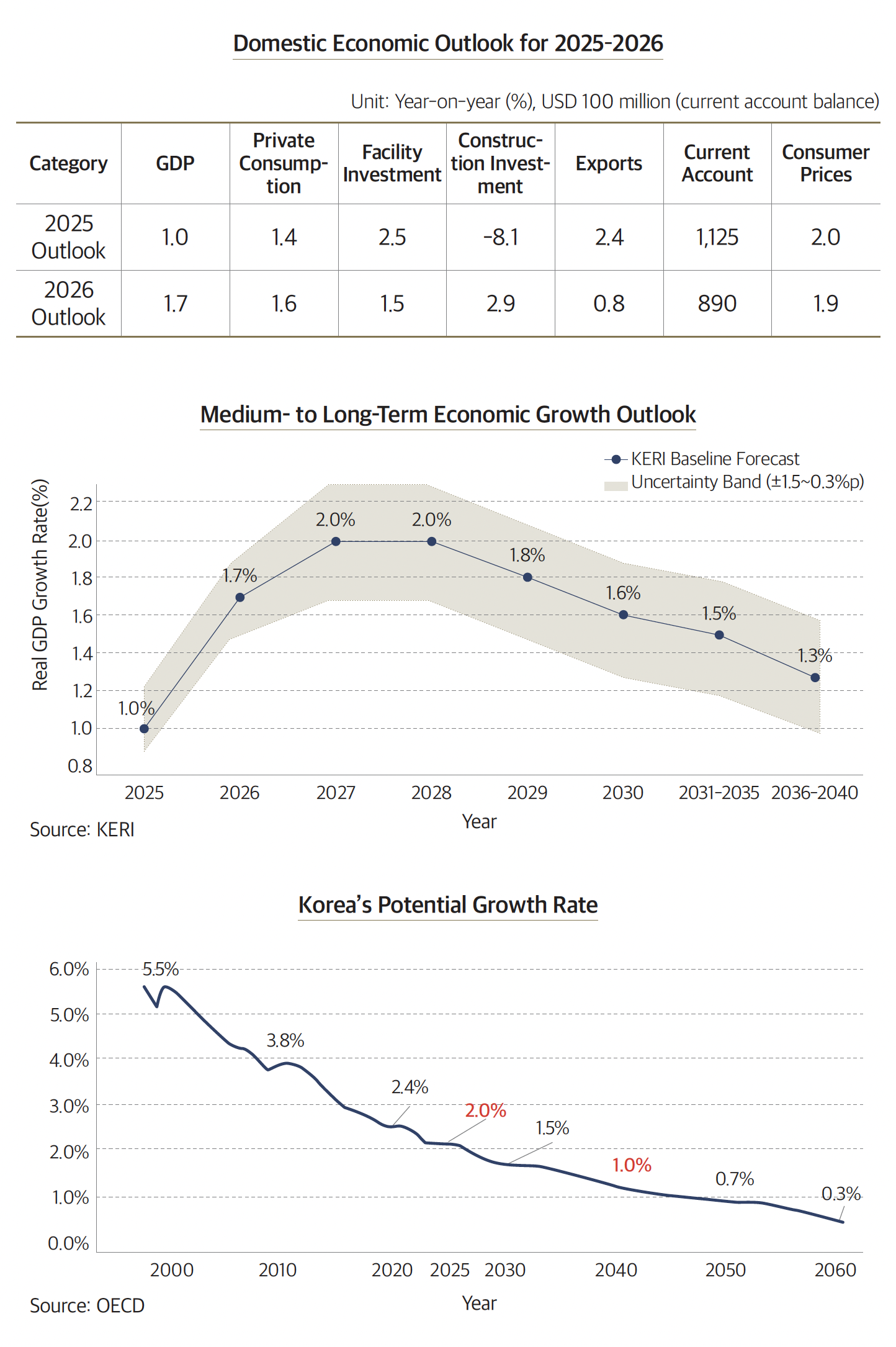

GDP Growth of 1.7%: Resilience After the Trough and Its Limits

In a December report, KERI projected Korea’s economic growth at 1.7% in 2026. This marks a recovery from growth of 1% in 2025, but remains below the estimated potential growth rate in the low 2% range. A key feature of this recovery is that it is not broad-based. Rather, it reflects a concentrated recovery amid industrial differentiation.

Exports are expected to grow by 0.8% overall, but performance will vary significantly by sector. Demand continues to expand for AI semiconductors, automotive semiconductors, and power semiconductors. Shipbuilding, defense, and secondary batteries are also benefiting from solid medium- to long-term order backlogs and policy-driven demand. In contrast, manufacturing sectors such as petrochemicals, steel, and machinery face a limited recovery due to global oversupply and the burden of tariffs and regulations.

Facility investment is projected to increase by 1.5%. While technology investment-focusing on semiconductors, AI, and automotive electronics- investment conditions in non-IT manufacturing are unlikely to fully recover amid uncertainty surrounding interest rates, exchange rates, and demand.

Private consumption, projected to grow by 1.6%, is expected to recover gradually on the back of price stability and sustained employment. However, debt burdens and fixed expenditures, including education and housing costs, are likely to cap the upside. Construction investment, projected at 2.9%, is expected to rebound following adjustments in project finance. This recovery, however, can be characterized as a normalization focused in industrial facilities and SOC, rather than a broad-based expansion.

Possible catalysts to growth include the potential reacceleration of the semiconductor supercycle, stronger-than-expected momentum in the United States economy, and expanded investment in SOC and industrial facilities. Conversely, trade risks involving the United States and Europe, entrenched low growth in China, residual burdens from project finance restructuring, and heightened volatility in the Korean won may constrain growth.

Taken together, the recovery expected next year can be characterized as a combination of foundational recovery and the early stages of structural transformation.

Shifts in the Financial Landscape: Rising Tensions Amid Expectations of Easing

A defining feature of the 2026 financial market landscape is that policy is expected to ease, but market tensions are unlikely to dissipate quickly. The United States 10-year Treasury yield is showing downward rigidity within a range of 4.3%–4.7%, as fiscal conditions, government bond supply, and technology investment continue to limit declines in interest rates.

At the same time, the depletion of reverse repo2 balances which have supported global liquidity, has further heightened market sensitivity. In markets without sufficient buffers, single factors such as government bond supply and demand, policy announcements, or geopolitical events tend to be transmitted rapidly across bond, equity, and foreign exchange markets. While expectations surrounding the AI rally and technology stocks remain intact, valuation pressures and vulnerabilities in credit markets remain. As a result, the pattern of relatively high volatility despite lower interest rates is likely to persist into next year.

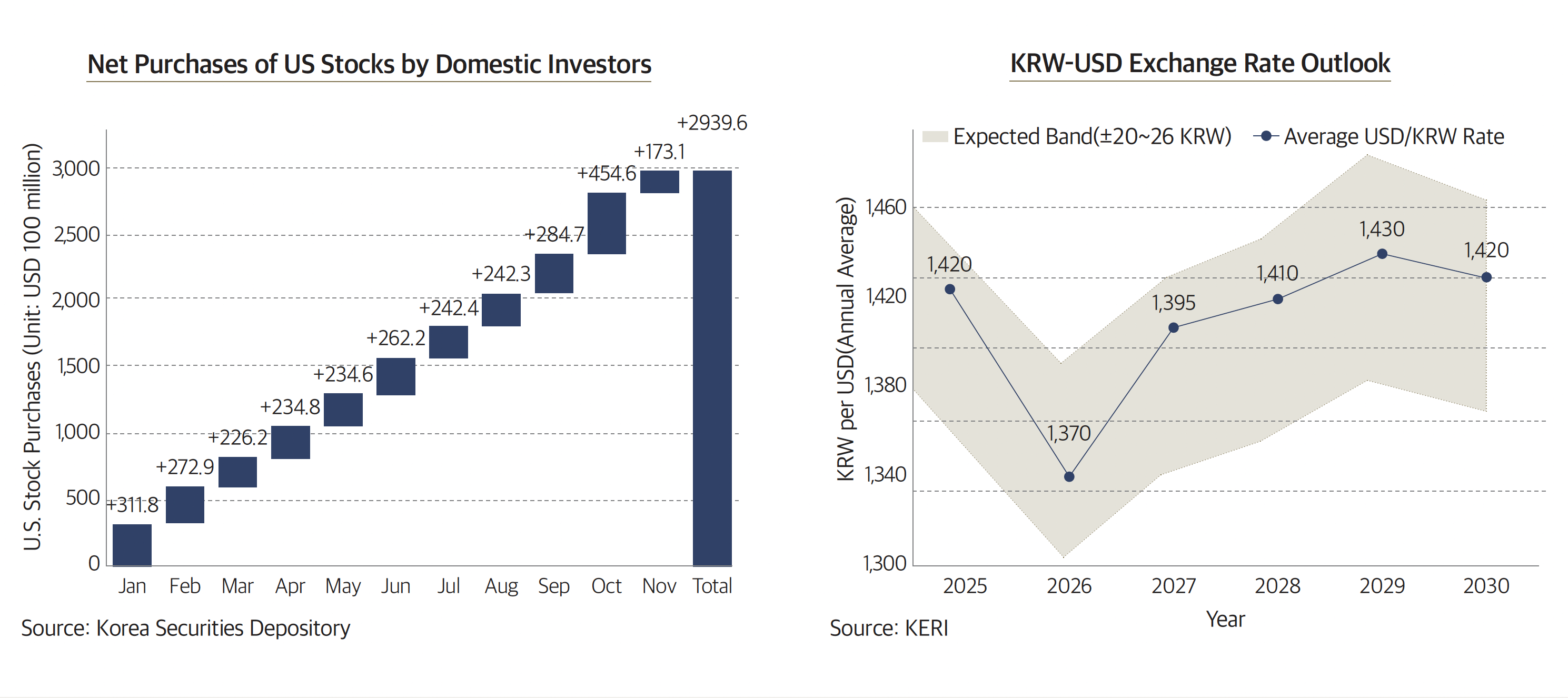

These shifts are already affecting Korea. Since October 2025, foreign investors have been reducing their exposure to Korean equities and bonds, increasing short-term selling pressure on the won. During the same period, domestic investors have expanded investment in U.S. stocks, ETFs, and U.S. Treasuries, boosting the demand for dollars and contributing to a rise in the exchange rate to the KRW 1,470 range. As large-scale foreign capital outflows exceeding USD 2.5 billion coincided with stronger domestic dollar demand, the KRW-USD exchange rate tested upper levels at a pace faster than suggested by economic fundamentals.

Essentially, the 2026 financial landscape is one of persisting tensions despite the potential entry into an easing phase. Against this backdrop of structural change, the KRW-USD exchange rate is likely to fluctuate within a range of KRW 1,370 ± 40 in 2026. Volatility, rather than direction, is expected to emerge as the more important variable. Even if the policy rate stabilizes at around 2.50%, structural tensions in global financial markets will remain a cost factor that will continue to be absorbed by the Korean economy in 2026.

- 2.Reverse repo: A transaction in which financial institutions place short-term liquidity with the Federal Reserve and receive interest using government bonds as collateral. It serves to absorb excess liquidity in the market.

Industrial Restructuring: A Clear Shift in the Balance of Power

Industrial restructuring in 2026 is significant not only because of widening differences in recovery across sectors, but because the very systemic conditions that determine competitiveness are undergoing change. Technology-intensive industries such as semiconductors, automotive electronics, shipbuilding, and batteries are strengthening their expansion base as global technology demand converges with policy support. Semiconductor exports increased by 43.9% in 2024, accounting for 21% of total exports. Shipbuilding and defense have also seen order backlogs rise by 15%–20%, supporting continued medium-term growth momentum. In contrast, manufacturing sectors such as petrochemicals, steel, and machinery face limited prospects for a clear rebound under the combined pressure of oversupply, regulation, and price competition.

This widening gap reflects not only differences in demand, but also the fact that regulatory and institutional changes in 2026 are being translated into tangible cost increases and competitiveness pressures. The E.U. Carbon Border Adjustment Mechanism (CBAM)3 has entered the carbon certification and pricing phase this year. At the same time, the IRA and the CHIPS Act are tightening supply chain and rules-of-origin requirements, directly constraining Korean firms’ investment decisions and supply chain strategies.

Domestic conditions are also reinforcing structural change. Demographic and labor market shifts, including an average annual decline of −0.7% in the working-age population between 2026 and 2030, combined with widening gaps in infrastructure and costs between the capital region and non-capital regions, are likely to further amplify differences in sectoral resilience.

Ultimately, 2026 will not be a year in which all industries recover together. Rather, growth paths will diverge across industries and firms, depending on how quickly they adapt to a new operating environment. Marking a turning point, 2026 will be a year that reshapes relative competitiveness for the years ahead.

- 3.CBAM: An EU system that imposes costs on imported goods based on carbon emissions generated during production, targeting imports that circumvent internal carbon regulations. The mechanism aims to prevent carbon leakage and protect domestic industries.

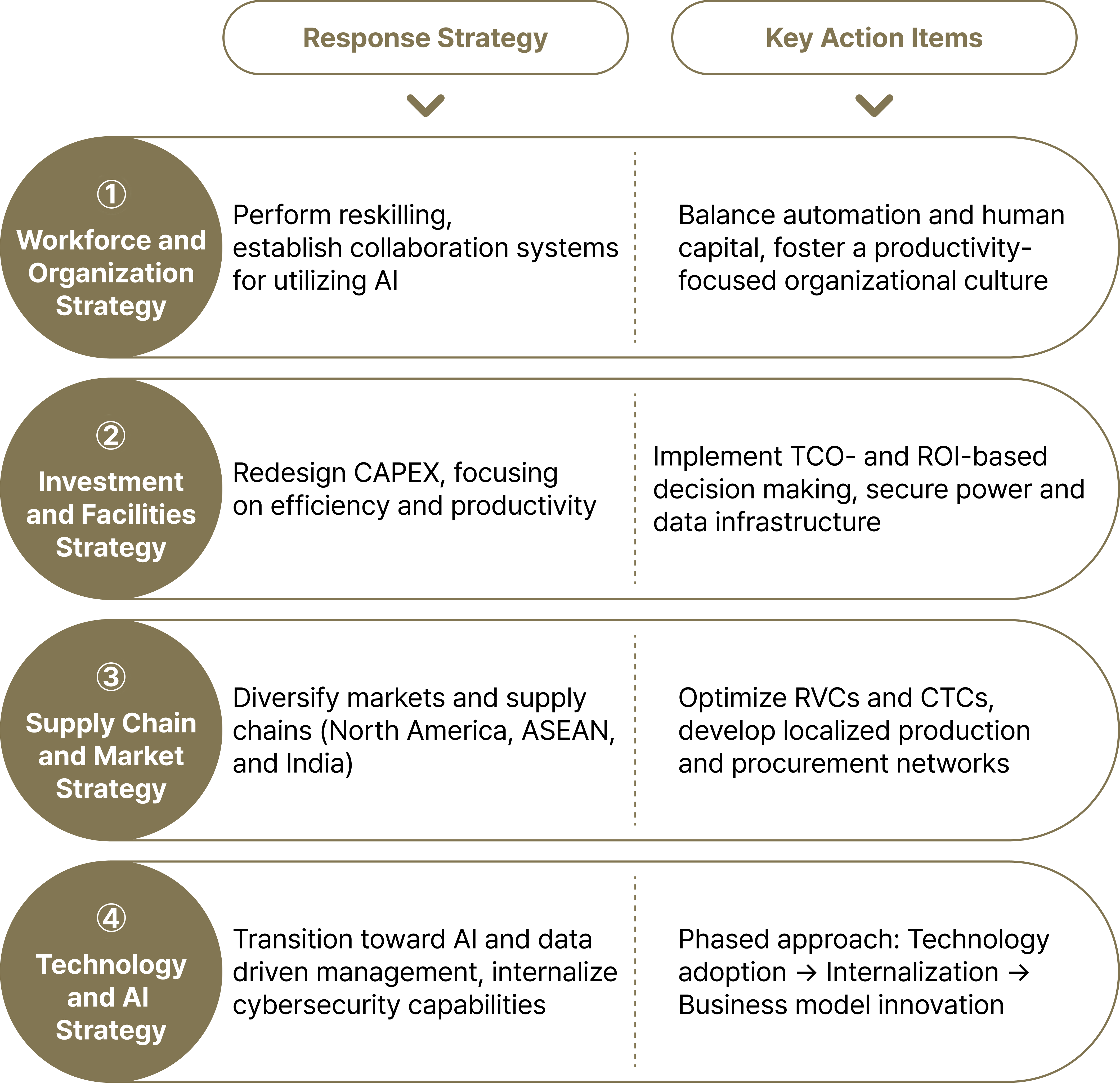

Firm Strategies in 2026: Steering Korea’s Next S-Curve Growth Pathway

The year 2026 marks a period of realigning growth engines for the coming decade. Opposing forces intersect in 2026: constraints such as population decline, rising costs, and tighter regulation exert downward pressure, anchoring growth around the 1% range, while expansion in sectors such as semiconductors, AI, shipbuilding, and defense presents firms with a rare opportunity to enter a new S-curve. The choices and responses made at this juncture will shape whether the Korean economy will remain locked in low growth or shift onto a trajectory that restores growth potential. Decisions on technology investment and the pace of enhancing internal productivity are ultimately firm-level strategies. However, these choices will effectively determine Korea’s growth path over the next five years.

Economic change may be hard to truly perceive from short-term performance metrics, but with directionality it manifests as widening gaps in long-term outcomes. The year 2026 is a period for resetting direction. The investments and adjustments during this period will shape the next phase of corporate growth and determine whether the Korean economy successfully enters a phase of S-curve growth.